An exchange-traded fund (ETF) is an investment fund that invests in a basket of stocks, bonds, or other assets. ETFs are traded on a stock exchange, just like stocks. Investors are drawn to ETFs because of their low price, tax efficiency, and ease of trading.

Because of its genesis as an index tracker, the ETF is widely associated with cheap, passive investment strategies. The vast majority of the industry’s USD9tn of assets are indeed in such vehicles, including USD320bn* in the top five U.S.-based robo advisors (*includes non-ETF products).

Robo advisors are digital platforms that provide automated financial planning. They offer plug-and-play, low-cost investing options – typically via passive, ETF-based portfolios – to retail investors.

The empowerment of retail investors and increased awareness of ETF investing via robos is a positive trend. Yet this obscures the fact that the ETF has evolved into much more than just a next-generation passive fund.

Like robos, Alphalytics Quant Multi-Strategy (AQM) uses ETFs.

Unlike robos, AQM is not a plain-vanilla ETF portfolio.

The below three tables highlight key features of AQM vs a leading Asia-based robo advisor.

____________________________________________________________

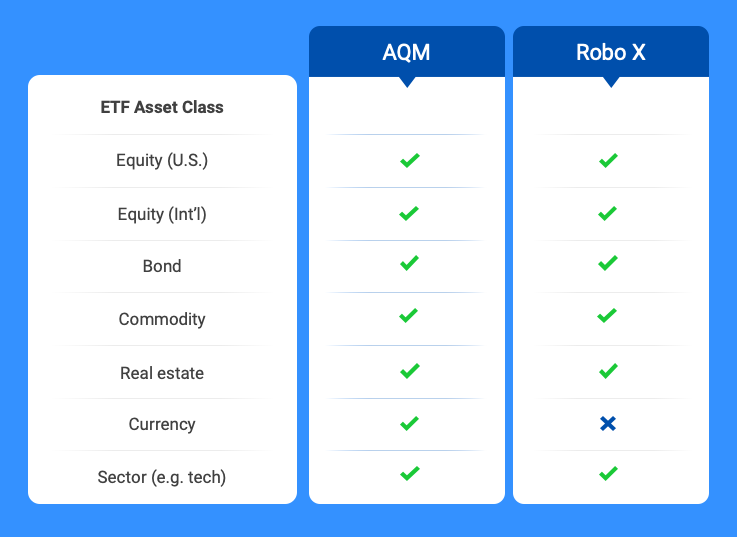

ETF Asset Class

Source: ACM Research

This is a common, universally-accessible list of asset classes. No surprise here that both AQM and Robo X choose to invest in these assets.

____________________________________________________________

Alternative ETF/ETN

Source: ACM Research

The use of alternatives is a significant AQM differentiator.

Most robos offer long-only ETF portfolios and hedging is done at the asset class level. i.e. Use bonds as the anti-correlated asset class to equities.

AQM uses alternative ETF/ETN as Lego-like blocks to construct sophisticated trading strategies to both outperform and hedge. Learn more about alternative ETF/ETN here.

____________________________________________________________

Fund Constitution

Source: ACM Research

There is a lot to unpack in this third table. Let’s look at four categories:

i) Investment style

Modern Portfolio Theory, used by Robo X, was developed by economist Harry Markowitz in the 1950s; his theories surround the importance of portfolios, risk, diversification, and the connections between different kinds of securities. In essence, proper diversification of a portfolio can’t prevent systematic risk, but it can dampen, if not eliminate, unsystematic risk.

AQM’s multi-strategy investment style is analogous to experiencing a three-course meal. 30 ETFs (ingredients) are used, in varying degrees, across 33 different trading models (dishes). These trading models are designed by the Portfolio Manager and are subsets of time-tested investment strategies (courses).

For more, see also this article “Multi-strategy hedge funds show way forward for industry” by the Financial Times (Sep 30, 2020; paywall content).

ii) Target CAGR

AQM uses a multi-strategy approach to target 25 percent CAGR in the long run.

Robo X offers a range of portfolios with varying risk-and-return profiles – none seek 25 percent annualized returns.

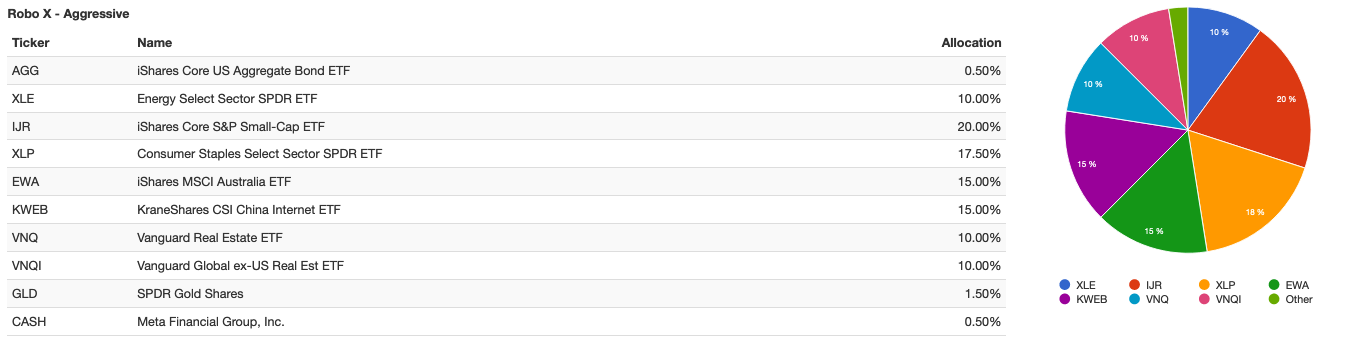

Using the ETF data from Robo X’s website — plus good faith allocation estimates — my attempt at backtesting Robo X’s most aggressive, mostly-equities portfolio matches its published 10-year, 8.3 percent CAGR projection – Robo X labels this at a 75 percent confidence level to achieve; and at a 5 percent confidence level to achieve, Robo X states that this aggressive, mostly-equities portfolio seeks a higher 20.6 percent CAGR over 10 years.

Sources: Robo X website; allocation assumptions by ACM Research

My observation is that Robo X’s CAGR targets are very reasonable and within industry expectations for long-only ETF portfolios.

iii) Target drawdown

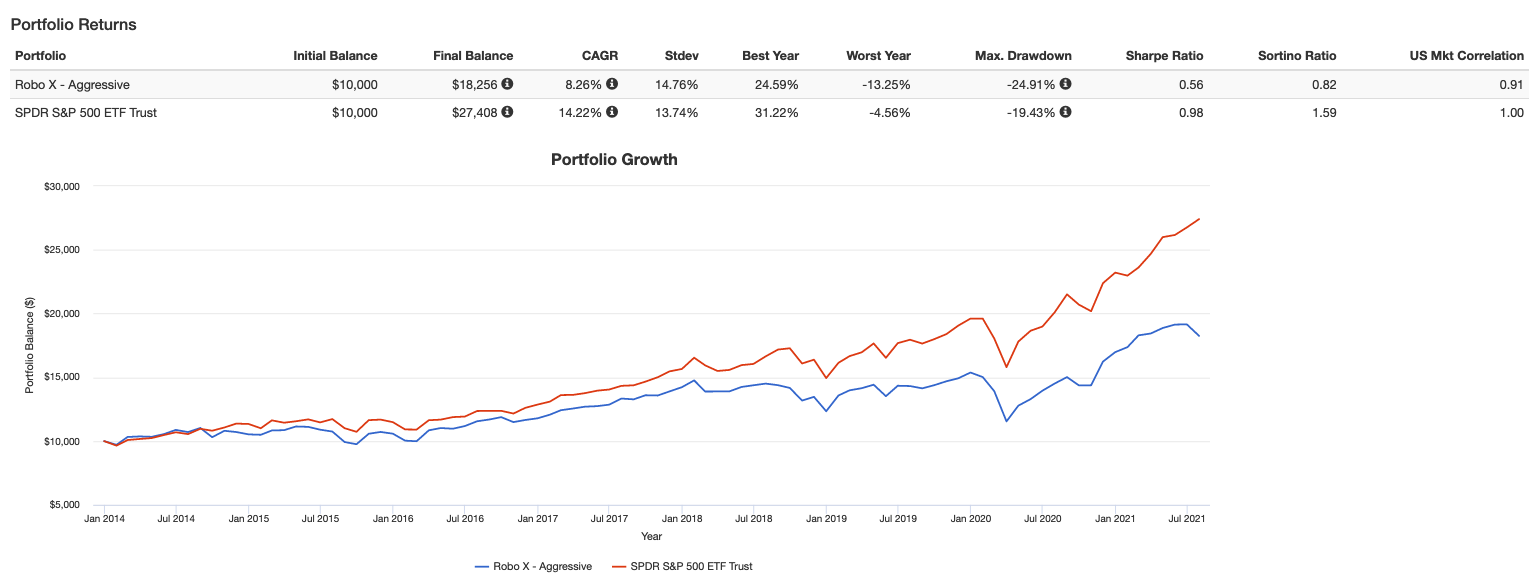

AQM targets a 15 percent drawdown (maximum cumulative monthly).

Robo X is not highly specific about its drawdown perimeters – understandably so as most retail investors will not require this level of granularity. My best attempt at modelling its drawdown is a 25 to 30 percent annual drawdown which matches Robo X’s broad guidance.

Source: ACM Research

This backtest result starts from 2014 because some of the ETFs listed on in Robo X’s aggressive portfolio was incepted only in 2014.

iv) Fees

Robo X’s 0.2 to 0.8 percent fixed annual fee is representative of robo advisory pricing.

A typical hedge fund charges 1 to 2 percent fixed annual management fee and 15 to 20 percent performance fee. AQM does not charge a management fee which is a significant cost saving for investors.

____________________________________________________________

Conclusion

Robos are at the frontier of making investing easy and accessible to the wider public; and the ETF is their instrument of choice to construct a variety of simple yet effective portfolios. Having looked at several leading platforms, I’d observe that the risk-and-return profiles offered by Robo X is fairly representative of most robo advisories.

The purpose of this post is to acknowledge investor’s common understanding that the ETF is a cheap, passive investment instrument typically associated with robo advisors; and to shift that reference point to appreciate the depth and goal of AQM’s investment strategy.

If ETFs are Lego-like blocks, then robo advisors are avid Lego builders of uncomplicated trading models, while AQM is a Lego Master Model Builder.

____________________________________________________________