According to a 2020 report, over a 15-year period, nearly 90% of actively managed investment funds failed to beat the market.

In the past decade, the S&P 500 has delivered 13.62% CAGR. And the S&P 500 posted its best 12-month performance in history between Mar 23, 2020, and Mar 23, 2021, gaining 74.8 percent. (For more about the S&P 500, see this post.)

Hence, most investors are indeed better off investing in passive index funds.

“By periodically investing in an index fund, the know-nothing investor can actually out-perform most investment professionals.”

-Warren Buffett

At the same time, according to Statista and Pensions & Investments, at the end of 2020, hedge fund AUM was at a record USD3.8 trillion.

This tells us that, for a certain group of investors, there is a good product-market fit – someone is obviously still writing cheques to hedge funds.

What do these investors know about hedge funds that the average accredited investor do not? More on point, how do institutional investors think about the investment process that is different from the individual investor?

_______________________________________________________________

1. Instruments serve a specific purpose.

Say an investment committee is given an investment mandate of 8 percent annual returns for the next three years. As they survey the universe of instruments that fit their mandate, what might be one element that is in the back of their minds?

Predictability.

Not in the sense of absolute, steady returns. But a thoughtful consideration of the instrument’s return-to-risk profile.

I heard a podcast interview of a Chief Investment Officer receiving a call from his external fund manager specializing in real estate. The fund manager shared his views that the market might be on the downturn and recommended that the CIO consider cashing out on some real estate investments and holding back on others.

The CIO’s reply: Stay the course as previously discussed. We have taken into account the cyclical nature of the various allocations in our overall portfolio, including real estate. We are fine to ride the cyclical nature of our allocation to real estate. Other instruments in our portfolio have been selected to hedge the real estate cycle.

Lesson: An informed investor is aware that instruments are subject to cyclical peaks and troughs – and plan ahead accordingly.

Specific to hedge funds, a key value proposition is the targeting of risk-adjusted returns: That investing is not about return, it is about the balance of return and the risk taken to earn that return. Alternatively, it could be a market-neutral fund that seeks alpha away from the equity market.

To that end, select classes of well-managed hedge funds could well be one of the predictable instruments in a portfolio – due to the quantifiable nature of the trading strategy.

_______________________________________________________________

2. Know the reward-to-risk ratio

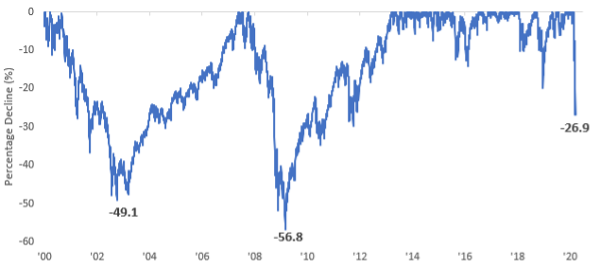

Ask any portfolio manager what this graph is and they will immediately recognize it as a maximum drawdown chart.

Source: S&P 500

Most investors are aware that risk is inherent with any investment.

Professional money managers quantify risk using maximum daily drawdown: A peak-to-trough decline during a specific period. See the chart shows that the S&P 500 maximum drawdown was 56.8 percent.

In the past 20 years, the S&P 500 had a 5.90% CAGR. Hence, we derive the simple yet useful reward-to-risk ratio of 0.10 (5.90% CAGR / 56.8% drawdown) for the S&P 500.

For every unit of risk, the S&P 500 in the past 20 years has achieved 0.10 unit of gains.

_______________________________________________________________

3. Large drawdowns are hazardous to wealth

Source: Alpha Architect

Both investment portfolios achieve 7 percent annual returns. The bar graph on the left experiences a 50 percent drawdown; it will take 11 years for the portfolio to recover.

Conversely, the investor on the right experiences a 15 percent drawdown; recovery takes only 3 years.

When aiming for high performance, playing great defense is just as, if not more, important than playing great offense.

_______________________________________________________________

4. Do not chase past performance

The reason is simple: Performance drivers are period-specific, hard to predict and unlikely to be repeated in the future. Investors who commit to a particular investment style that has proven itself by way of recent past performance might be vulnerable to a cyclical turn of events.

Studies show that when a particular investment approach excels in a certain macro environment, it tends to underperform the following period/year when the macro environment changes.

In sum, betting on one style over the other based on the magnitude or duration of its past outperformance in any given timeframe is not a sound strategy for maximising returns. More in this post.

_______________________________________________________________

Conclusion

Hedge fund investment is a two-way street.

Credit: Alpha Architect

After all is said and done in terms of due diligence, even institutional investment teams will need to take a small step of faith in the investment strategy – it is not feasible to uncover every single red flag.

As for the individual accredited investor, it is beholden on the fund to do a good job of communicating how investing works, what their strategy is, what they should expect as an investor, and how to deal with inevitable volatility and cyclicity.

At the same time, from the perspective that it is a privilege for an individual investor to have access to a market-beating hedge fund, it is in the investor’s own best interest to get to know the characteristics of a fund.