Today’s most captivating technology is blockchain — the underlying technology behind cryptocurrency — which could be a game changer for the global economy.

Still in its early stages, mainstream blockchain integration may still be years away, yet some view it to be as ground breaking as the adoption of the internet. Just as the internet upended how we share information, blockchain has the potential to revolutionize how we exchange value, transfer ownership, and verify transactions.

Blockchain technology is currently being piloted across industries, spanning from financial services to manufacturing. Other sectors, like retail, healthcare, supply chain, and real estate, are also beginning to experiment with potential applications. In the long run, blockchain may enable a transformation of operating models across industries.

_______________________________________________________________

Here are free primers that I have curated to orientate novice learners:

- What is blockchain technology? by IBM. Includes a free copy of “Blockchain for Dummies.”

- Tokenization, Explained by Cointelegraph

- Tokenization of Assets: DeFi by EY

I’d encourage you to read the above primers in order to get the most of the rest of my commentary.

For the intermediate learner, the Hidden Forces podcast covers a range of topics. Its host, Demetri Kofinas, excels at long-form, deep-dive interviews with subject matter experts. Check out his episodes on crypto for in-depth exposition.

_______________________________________________________________

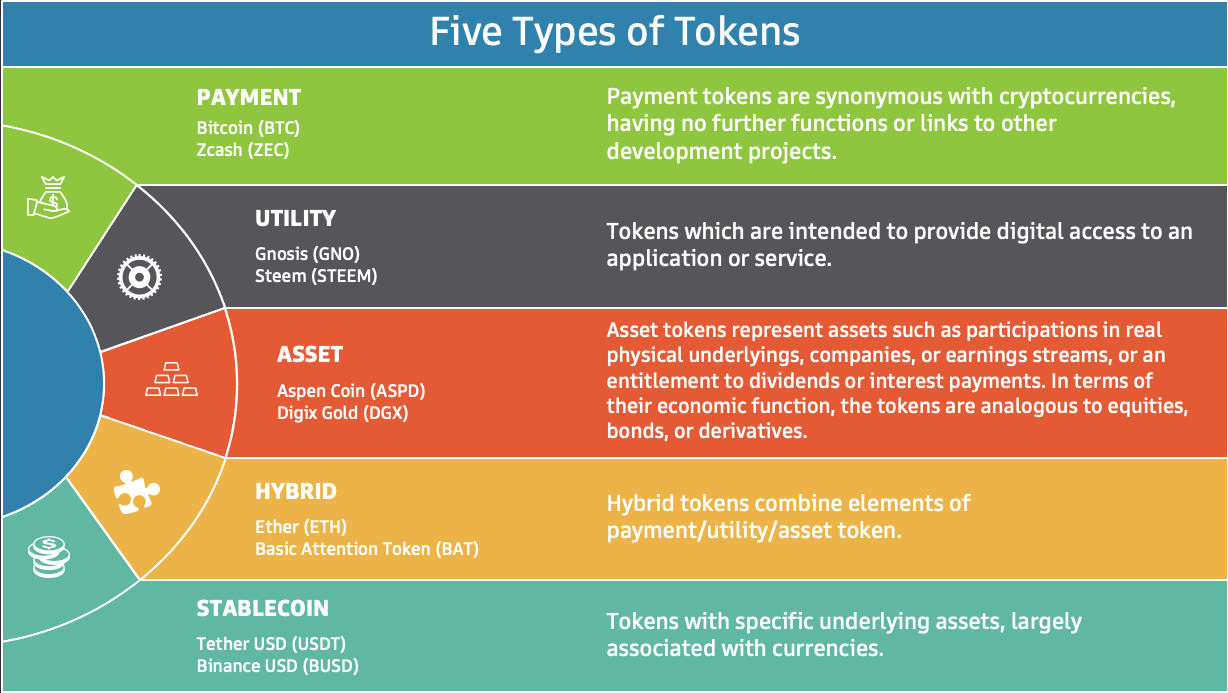

As an overview, these are the five broad categories of tokens:

Source: EY and ACM Research

Four of these five tokens (payment, utility, hybrid, and Stablecoin) may be listed on a digital exchange; that is referred to as an initial coin offering (ICO).

Asset tokens may also be listed on a digital exchange — a key difference is that a digital exchange that offers asset tokens is regulated. When listed, it is referred to as an securitized token offering (STO). (You may also hear it referred to as an asset-backed security).

_____________________________________________________________________________________

IPO, STO, ICO

An easy way to understand digital exchanges (STO and ICO) is to compare them against the traditional stock exchange (IPO).

IPO (traditional exchange)

NYSE, SGX, and HKEX are traditional, regulated stock exchanges where IPOs occur.

STO (digital exchange – regulated)

Security token offerings (STOs) take place on digital exchanges. Think of a digital exchange as a traditional stock exchange but instead of stocks and bonds, investors buy crypto-assets (i.e. tokens) that are tied to (i.e. securitized by) real-world assets.

The most prominent digital exchange offering STOs is currently tZERO. As an example, on tZERO, Aspen (ASPD) is the security token representing fractional ownership in the St. Regis Aspen Resort — a five-star 179-room hotel in Colorado.

ICO (digital exchange – less regulated)

In the final category, the most loosely regulated – arguably not regulated – digital exchanges are where initial coin offerings (ICOs) are offered.

Simply put, this is where one goes to buy Bitcoin (BTC) and Dogecoin (DOGE) – the value of which are fiat (i.e. unto itself) and not tied/not securitized to an underlying real-world asset. (Given the lack of regulatory oversight, one might laud the democratization of capital markets by easily launching a personalized, hypothetical $JohnLee coin.)

The most prominent digital exchange offering ICOs is Coinbase. Given Coinbase’s current dominance, should it progress to offer STOs? Not necessarily. Because it takes significant effort and money to scale the evolving regulatory walls, Coinbase might be better served, in the middle run, to capture value in the ICO market.

When asked about this in Mar 2021, Coinbase CFO Alesia Haas noted:

“Could we do a security token? And as we evaluated those options, what we came up with was the security token infrastructure is not quite there, that we didn’t have the opportunity for all investors. Many institutional investors can’t participate in security tokens, and we didn’t have enough broker dealers that could trade it to provide liquidity to the market. And we, Coinbase, didn’t have the right licenses or the right foundation to be able to offer that.”

_______________________________________________________________

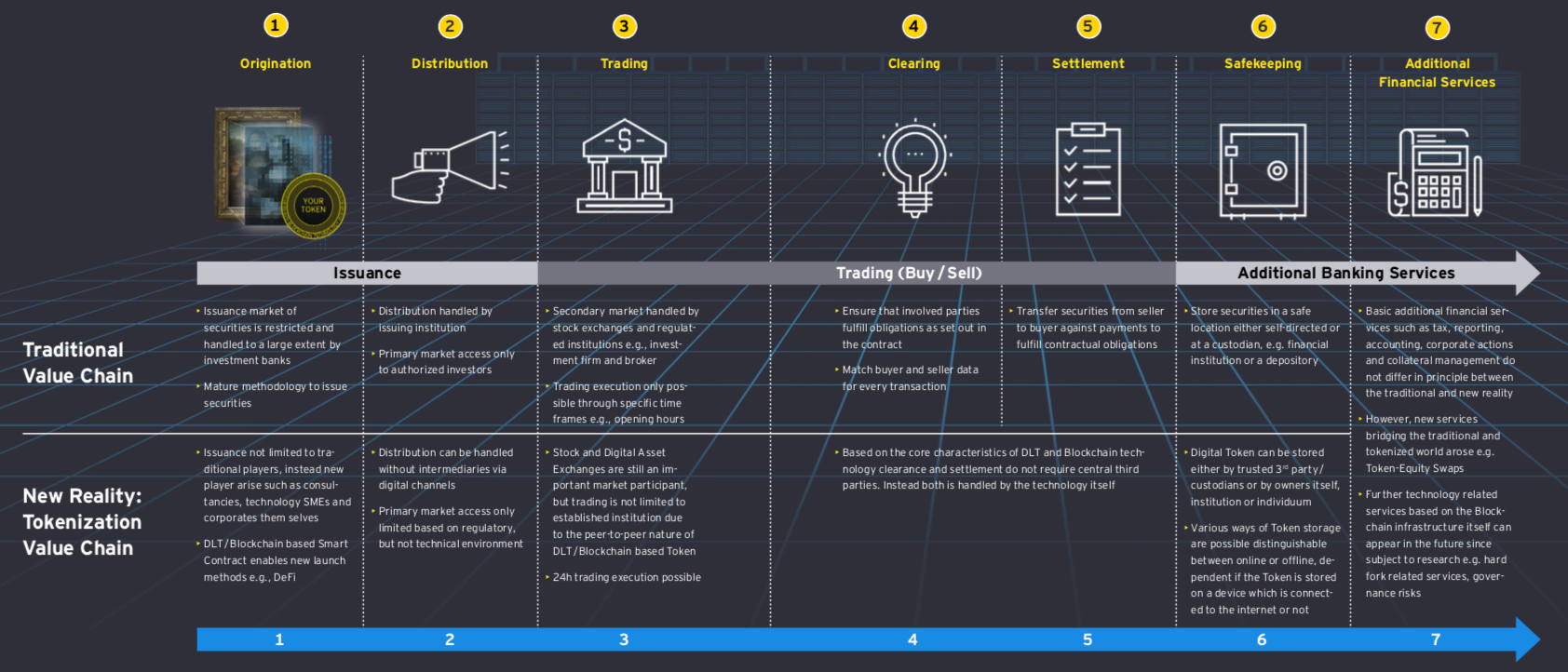

Global STO landscape

Funds and asset management firms sit at the beginning of the commercial value chain. i.e. origination and issuance. Hence, we shall look at asset-based tokens.

Source: EY

To supplement your understanding of STOs, here are some curated commentary and insights:

- Is 2021 the Year of the Security Token? by Investopedia

- STOs: The What, Why, Who and How by Tanner DeWitt Solicitors

- Are token assets the securities of tomorrow? by Deloitte

By now, you would have observed that the progress of digital exchanges offering STOs is tied to the hip with traditional securities regulation. (Not considering off-shore jurisdictions such as Cayman and Seychelles.) As such, here is a useful listing of each country’s legal definition of digital securities and security token.

_______________________________________________________________

STO Digital Exchange Landscape in Singapore

Overview

Based on ACM Research, Singapore is a leader in the region to both endorse a regulatory sandbox and authorize digital exchanges – Singapore is, as of this writing, currently a step ahead of the other regional financial hubs Hong Kong, Korea, and Japan.

Security tokens in Singapore currently fall under the country’s Securities and Futures Act (SFA). However, unlike other countries, Singapore has an added legal dimension when it comes to security tokens. Specifically, the Payment Services Act also has jurisdiction over some cryptocurrencies as well – there are currently approx. 100 entities that, as of 28 July 2020, were authorized as providing payment token service.

Simply put, the Payment Services Act (PSA) governs ICOs and cryptocurrencies: An entity needs to be licensed under the PSA in order to trade in and offer payment tokens, including the buying and selling of crypto-assets such as BTC.

As for asset/security tokens, a CMS license is needed and STOs are currently restricted to accredited investors.

As a related side note, on the banking front, four entities in Singapore were awarded digital banking licenses in early Dec 2020.

Digital token legislation

The Monetary Authority of Singapore (MAS) has set up a sandbox with companies to operate security token exchanges and platforms. After working with the market participants, the MAS released a guidance paper for Digital Token Offerings in May 2020.

An entity in the MAS sandbox operates with a lighter regulatory touch as it works on its proof of concept; MAS does not endorse the commercial viability of entities in the sandbox.

STO framework

The MAS guidance paper defines security tokens as traditional securities based on Singapore law, and therefore must follow all similar regulations and requirements to comply. Using multiple example scenarios, MAS broadly covers all aspects of issuing a security token ensuring explicit clarity for the industry.

__________________________________________________________________

STO digital exchanges in Singapore

There are currently seven digital exchanges in Singapore: The first four are fully operational; and the last three are pending exit of MAS sandbox in 2H2021.

Relative to other financial hubs in Asia, Singapore has adopted a forward-looking regulatory stance for digital exchanges to experiment and go-to-market.

These digital exchanges are also on the forefront of shaping STO backend functions: KYC/AML, trading, clearing, settlement, and safekeeping – in the long run, this benefits investors as operational and cost efficiencies will be realized as the traditional ecosystem adapts to the new reality.

From commercial and distribution perspectives, leverage of the network effect is critical to these firms’ success – size matters! How many of these seven firms will be left standing in 3 to 5 years’ time? My contention is that three of these firms will thrive in different and overlapping market segments.

__________________________________________________________________

What are the conditions and pitfalls that these digital exchanges can expect to navigate?

Demand side

- Tension between targeting accredited investors (AIs) vs mass affluent. Fractionalization of previously inaccessible assets is one key value proposition for STO customers. At the moment, most STOs are restricted to accredited investors (individuals and institutions) who might not perceive sufficient value in fractional investments to move their trades on to an emerging digital exchange. Put another way, serving two different masters – accredited vs retail – is challenging because the two segments’ perception of value are very different.

- Early adopters are speculators, not investors. Crypto-assets are currently associated with speculative investors with high-risk appetite, looking to turn a quick profit. (Think Dogecoin). Plus, investor awareness and trust around STOs are low and educating investors takes significant time and marketing dollars.

- Sizing up total addressable market. What value to the investor are digital exchanges bringing to the table that is different from say a Fundsupermart? The clearer a digital exchange’s value creation proposition, the more in focus the addressable market, and the more apparent the products to be curated onto the platform.

Supply side

- Identifying product-market fit. A successful digital exchange is the one that recognizes, articulates, and leans into a business model that maximizes its unique network effect. Investors are spoilt for choice of platforms: Why should an investor switch to your digital exchange over another platform (digital or traditional)?

What is each digital exchange’s commercial niche and product-market fit? Thoughtful investor segmentation matters and, in turn, informs product/asset curation.

For instance, to succeed as a platform, Jeff Bezos picked books:

“I picked books because there were more items in the book category than in any other category. And so you could build universal selection. There were 3 million in 1994 when I was pulling this idea together — 3 million different books active in print at any given time. The largest physical bookstores only had about 150,000 different titles. So that’s why books.”

- Show me the cost savings. Are STOs old wine in a new skin? For all the talk about efficiencies, accessibility, liquidity, and transparency, how are STOs better (cheaper? faster? more liquid?) than the offerings on traditional exchanges? Most investors are likely to sit on the side line, waiting for the adoption curve to play out. In the meanwhile, first mover digital exchanges need to cope with high sunken costs and stakeholder/shareholder expectations in order to be amongst the last ones standing.

- Managing the known and unknown counter-party risks. Regulated digital exchanges are on the leading edge of compliance and KYC/AML approaches and execution. These subject matters are not new; how to efficiently scale compliance and KYC/AML – and not let known unknowns undermine the exchange – is.

Brief note on taxation

- Entity taxation: For income tax purpose, IRAS views a payment token as an intangible property. Consequently, where a business receives payment tokens for the goods or services it has provided, the business would be taxed on the value of the underlying goods provided/services performed. See this IRAS summary and MAS guide.

- GST: GST it not levied. See this summary and this MAS guide.

_________________________________________________

Conclusion

Tokenized assets are likely to flourish – potentially as a complement to current traditional assets in the financial world.

Tokenization of assets are already taking place in forward-looking jurisdictions like Singapore, Switzerland, the U.S. As a catalyst, it is deeply transformative for the entire financial services ecosystem: investors, originators, intermediaries, legal, and regulators.

Though whether STOs can deliver on one of its lofty promises to reduce inequity by democratizing access to investments would require purposeful regulatory engagement and commitment by intermediaries to build an equitable system.

In sum, tokenization is transformative, still in infancy stage, and market adoption will need time.

______

Additional credit: JPMorgan Chase news.