Over the last 30 years, the asset management industry has been disrupted by the growth of exchange-traded funds (ETFs).

In 2020, the assets managed by ETFs in the U.S. alone surpassed the USD5 trillion mark, amounting to about 17 percent of the total assets in U.S. investment companies. To date, more than 3,400 ETFs have been launched, covering broad-based indexes like the S&P 500 to niche investment themes such as cannabis, work from home, and COVID-19 vaccines.

As a systematic ETF strategy for accredited investors, AQM is most often misunderstood as either a robo advisor or a thematic ETF available for retail investors.

The purpose of this post is to flesh out three classes of ETFs (vis-à-vis AQM).

__________________________________________________________________________

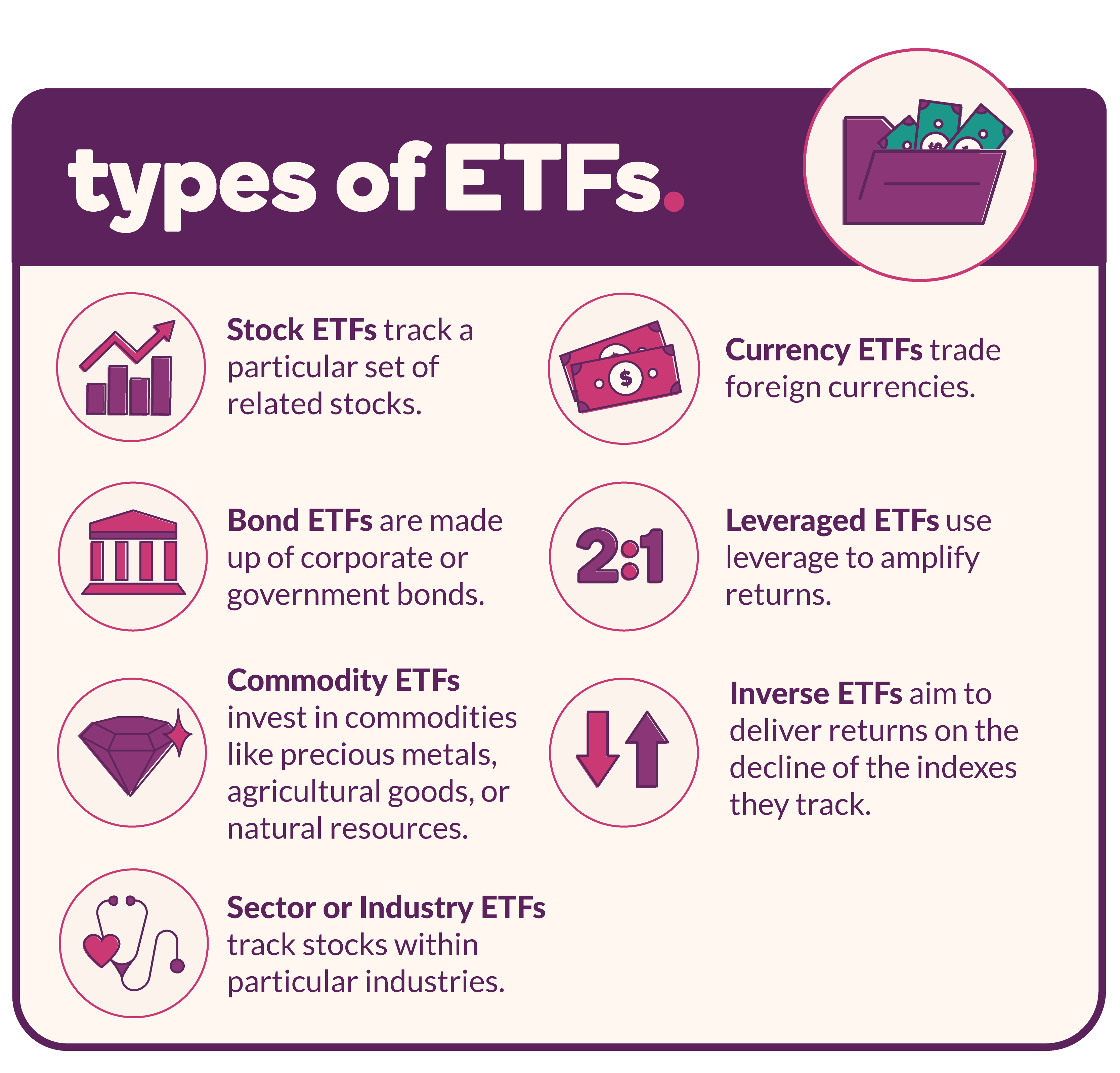

Primer on ETFs

Exchange-traded products (ETPs) are investment instruments whose objective is to replicate the performance of an index — in a similar manner to index mutual funds.

Unlike index funds, however, ETPs are listed on an exchange and are traded throughout the day — similar to stocks, the price of ETPs fluctuates day-to-day.

These funds are organized in several legal structures such as exchange-traded funds (ETFs), exchange-traded notes (ETNs), exchange-traded commodities, and index participation units (IPU).

Credit: Ally.com

The first U.S. ETF, SPY, was launched in January 1993. It tracked the S&P 500. SPY is currently the largest ETF in the world with USD350 billion in assets.

To browse the sheer number of available ETFs, ETFDB is a good place to start. (Fair warning that the number of ETFs and categories can get overwhelming rather quickly.)

ETFs can reproduce the performance of the relevant index in two ways. First, they can hold a basket of securities that, more or less, replicates the index (“physical replication”). Second, they can enter into swap agreements with financial institutions to have the performance of the index delivered by these counterparties in exchange for a fee (“synthetic replication”).

For more, see this FT article on How do ETFs work?

__________________________________________________________________________

Robo advisors

Robo advisors are low-cost, low-effort investment vehicles for retail investors.

A key value proposition for a robo advisor is its easy-to-use, plug-and-play approach to investing.

They are an excellent choice for newbie investors getting started because of their user-friendly design; and robo advisors prioritize the ease of customer onboarding and a fuss-free investment journey.

The minimum investment amount is low, there is often no lock-up period, portfolios are largely pre-determined (typically along the lines of aggressive, balanced, or conservative), and the holdings are transparent.

In contrast, AQM is a fund for accredited investors (AIs) because it holds a basket of undisclosed ETFs, including leveraged and inverse ETFs which are instruments, when used by a fund, the regulators restrict to AIs.

AQM trades ETFs in an intra-day frequency while most robo advisors buy-and-hold the underlying securities for weeks, months, or longer. In terms of frequency of trade, these are different investment approaches and neither is inherently better.

AQM seeks high performance that beats the market — no robo advisor targets 25 percent CAGR — and risk-adjusted return.

Like all of its peer funds, relative to a robo advisor, AQM has a higher minimum ticket size, a lock-up period, and a fee tied to performance.

For more about the rise of robo advisers in Asia-Pacific, see this Deloitte study. For a global robo adviser ranking (U.S.-centric), reference this site.

__________________________________________________________________________

Thematic ETFs

Thematic ETFs — the most popular nowadays being ARKK by ARK Invest — are not new: QQQ, launched in 1999, is a technology-themed ETF that tracks the NASDAQ.

This WSJ article provides a good summary of the pros (low cost and accessible) and cons (limited diversification and too trendy) of thematic ETFs.

The founder of ARK Invest, Cathie Wood, and her team have done an amazing job with outperformance and stellar marketing. So much so that she is literally moving markets when introducing a new Space Exploration ETF (ARKX).

For another point of view about ARK Invest, see below extract from a Barron’s writeup (Jan 4, 2021):

The funds have done it by owning a who’s who of innovative companies, including Tesla (TSLA), Square (SQ), Roku (ROKU), and Invitae (NVTA), and their success has attracted massive inflows. But the stock market gains might be unsustainable.

ARK Innovation is now 67% above its 200-day moving average, while ARK Genomic is 82% above it.

“The definition of parabolic is a trend that accelerates its steepness as it moves higher, which is what ARKK is doing presently,” Krinsky says. “This can continue in the short term, but we would be cautious on this ETF and many of its holdings as we head into 2021.”

True to this analysis, it is no wonder that ARKK, an all-equities ETF, dipped in early May 2021 as the technology sector cooled off.

AQM, on the other hand, is not a thematic ETF.

AQM is not limited to an investment theme. Instead, AQM is a multi-strategy, quant fund that trades 30 ETFs using 33 trading models across six classes of investment strategy (statistical arbitrage, trend following, momentum, long/short, etc.).

AQM is broadly diversified across asset classes and is a non-discretionary fund – daily trading decisions are not subjected to the Portfolio Manager’s subjective judgement – designed to hedge and outperform in various market conditions.

Conversely, ARK offers actively managed, equity-only ETFs; the ARK team does fundamentals stock picking to outperform the market.

AQM has holdings in equities, bonds, commodities, currency, etc.; and hedged trading models that seek upside participant and downside protection.

In sum, AQM and ARKK are different investment products for different customer segments with different risk-and-reward tolerances.

__________________________________________________________________________

Leveraged and Inverse ETFs

Beyond plain vanilla ETFs and thematic ETFs, leveraged ETFs are constructed using financial derivatives or debt to amplify the returns of an underlying index.

Think of these as ETFs on steroids.

On the one hand, these ETFs give the average investor easy, low-cost access to derivative instruments. On the other hand, these are double-edged swords that can lead to both significant gain and loss.

While a typical ETF tracks securities in its underlying index on a 1:1 basis, a leveraged ETF aims for a 2:1, or even a 3:1, ratio.

The first thing to note is that the 2:1 or 3:1 claim made by their issuers only apply on a daily basis and do not apply for long term investments.

For example, if the S&P 500 increases 10 precent over the coming one year, it is not reasonable to expect SPXL (3x leverage of S&P 500) to increase 30 percent during the same period.

Secondly, many, especially retail investors are not aware that leveraged, either long or inverse, ETFs suffer from volatility decay. Further recommended readings here.

Similarly, an inverse ETF is constructed by using various financial derivatives. However, an inverse ETF seeks to profit from a decline in the value of an underlying benchmark. Thus, inverse ETFs allow investors to make a profit when the market or the underlying index declines, without having to sell anything short.

Of the USD5 trillion assets managed under ETFs in the U.S., about USD 55.3 billion are leveraged and inverse ETFs by the two leading providers.

ProShares, the first issuer to roll out leveraged and inverse ETFs, has nearly USD36 billion in AUM in these funds.

Direxion, the number two issuer of leveraged and inverse ETFs, has 60 such funds holding USD19.3 billion in AUM. Its customer base for the products according to its President, Rob Nestor, is two-thirds “classic active trader” and one-third “tactically-oriented financial advisors, RIAs, and hedge funds.”

Furthermore, both Direxion and ProShares have plowed massive amounts of money and hours into providing education around the leveraged and inverse products they offer regarding how they work, in the interests of ensuring that investors understand the ins and outs of them and that they are more likely to have a good experience with the products.

__________________________________________________________________________

Conclusion

The great Warren Buffett said, “A low-cost index fund is the most sensible equity investment for the great majority of investors.”

To proof his point, Buffett won a 10-year bet that the S&P 500 will outperform a portfolio of funds of hedge funds, when performance is measured on a basis net of fees, costs and expenses.

To that end, ETFs are perfect vehicles for most investors.

For the motivated and informed investors desiring thrill, leveraged and inverse ETFs are readily available.

For instance, DIY investors can design strategies that capture volatility decay value by systematically shorting certain leveraged ETFs.

Conversely, investors can also design long only strategies that take advantage of leverages embedded in these ETFs to beat the market. See this post.

Though be forewarned: Beating the market is not easy. Always experiment with care.

___________

Citation: Credit to the ‘ETF Space’ paper for the above introduction and primer on ETFs.