Why consider a hedge fund?

Good hedge funds are a source of alpha diversification.

Most accredited investors have the luxury of choice and capital to diversify across both illiquid (PE/VC and real estate) and liquid (hedge fund) investments. In a well-designed, diversified portfolio, these assets would have varying maturity dates (i.e. staggered investment time horizons) and different periods of drawdowns.

Hedge funds add further diversification to a client’s portfolio and need not ‘take away’ allocation from illiquid investments.

Why invest in a new fund? Is it not better to invest in an incumbent fund with a longer track record?

Better performance is a primary benefit.

A standard disclaimer with marketing decks and performance summaries is that “past performance is not indicative of future results”. This has proven true over multiple academic studies: track records have little bearing on future outcomes.

Prior performance of individual funds is in fact statistically insignificant and carries virtually zero predictive power when it comes to forward-looking returns.

The fact is that smaller managers have been shown to consistently outperform their larger counterparts.

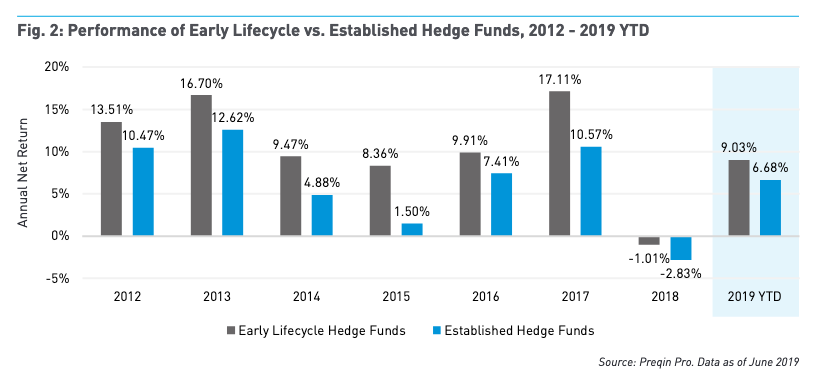

In addition, a Preqin-50 South Capital study (Oct 2019) shows the outperformance of new vs incumbent funds:

- Hedge funds early in their lifecycle have outperformed more established hedge funds by almost 4% on an annual basis over the period studied (2012 to 2019); and

- Over the 7.5-year period, the cumulative outperformance by early lifecycle managers relative to established managers is over 36%.

Source: Preqin

What the data suggests is that investors would have generated higher returns by investing in early lifecycle hedge fund managers.

These results suggest that investors can benefit from investing in early lifecycle hedge funds as part of a robust hedge fund program.

Source: Preqin

Why switch to AQM?

Alphalytics Quant Multi-Strategy (AQM) needs to offer a better risk-adjusted profile than the client’s existing product.

For each unit of risk, AQM has to target a better rate of return. If AQM’s risk-adjusted performance cannot beat a client’s existing private bank product, there is no reason to switch to AQM.

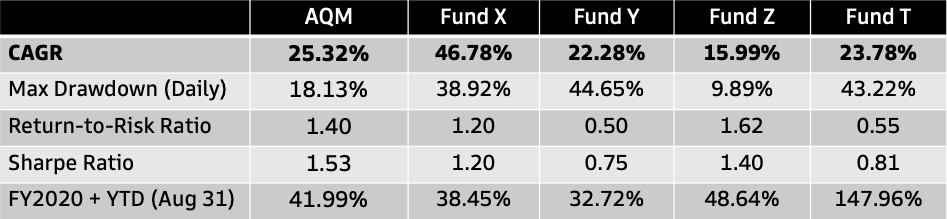

Tracked again 13 peer funds (top performers and award winners in Asia), AQM is ranked #3 in terms of FY2020 + YTD (end Aug 31) performance and has a decent Sharpe Ratio of 1.53. Thus far, the fund is delivering against our value proposition of high, risk-adjusted returns (i.e. a smooth return profile).

Source: ACM Research and BarclayHedge (top peer funds)

Summary

Incumbent private banks offer the halo of an established brand: Clients feel ‘safer and more secure’ when purchasing investment products from blue-chip entities – which is one reason why private banks are able to charge higher fees for mediocre performance.

Clients pay a premium for the brand halo, not necessarily for performance.

As a fully-licensed fund, AQM is subject to a similar level of scrutiny and regulation as funds offered by incumbents. And, pound for pound, the fund is delivering higher performance with lower fees relative to majority of private bank products.

As an early lifecycle fund, AQM is for the customer segment willing to forgo the brand halo in exchange for higher performance.

____________________________________________________________

Email hello @ alphalyticscm dot com for more about our investment strategies: (i) High performance targeting 25% CAGR and (ii) All Weather targeting better performance than equities with similar stability as bonds.