Executive summary

- AQM is up 7.88% in the month of June and up 6.58% YTD (Jan to Jun). In the past 12 months, AQM achieved 26.0% gross returns.

- After the Fed announcement in mid-June, US Treasuries raced higher which buoyed AQM’s YTD results.

- Investors are heading into the second half of the year weighing whether a recent acceleration in inflation is shaping up to be transitory, or the start of a longer-term trend that might force the Federal Reserve to pick up its pace of interest-rate increases.

- If US Treasuries continue its recovery, we expect AQM to have a strong 2021.

____________________________________________________________

Aligning investor expectations

The mid-year mark sparks a time for reflection on what has transpired and what the future holds.

AQM achieved 40.4% gross returns in 2020 – that was the sizzle that piqued investor’s interest. However, the fund’s flat performance in early 2021 raised some concerned eyebrows. Hence, it is incumbent on the AQM investment team to attempt to communicate its investment philosophy.

The unvarnished reason why AQM was flat (Jan to May) is the sustained drop in US Treasury prices – as straight forward as that. Behind-the-scenes, the investment strategy is working fine.

Consider this: Even though bonds dealt a material negative blow, if AQM did not have other sub-strategies protecting and holding up the overall portfolio, the Jan to May figures could have been rather dire.

This plainspoken answer triggers a handful of “why then didn’t you” inquiries. A common thread of this line of questioning presumes that AQM is a conventional long or long/short fund.

____________________________________________________________

Conventional vs quant

Conventional funds generally take a directional bet on the market: The fund manager has a point of view of where things (prices) are headed and adjusts (buy-and-sell) according to his/her interpretation and forecast.

When the year started, a conventional long-only fund manager might analyze the data and conclude, as Buffett did, that bond investors face a bleak future. The fund manager’s decision might be to dump US Treasuries; provide a macro trend commentary to investors; and list sound justifications to rotate out of bonds.

Most investors can relate to the above long-only blueprint — investors are hard wired to story create and to recognize a coherent narrative that rationalizes trading decisions.

This approach is diametrically opposed to a quant, multi-strategy fund’s investment philosophy. AQM views investing in terms of long-run statistics and probabilities, not directional bets based on subjective, short-run interpretation of data.

Quants rely on statistics and probabilities to make trading decisions. A quant fund manager does not purport to forecast where the market is headed (short run); instead, trading decisions are based on the highest possible probability of an outcome (long run). (The absence of a point of view about the short run often perturbs investors who are conditioned to receive descriptive and prescriptive market analysis from conventional fund managers.)

____________________________________________________________

The bond story thus far

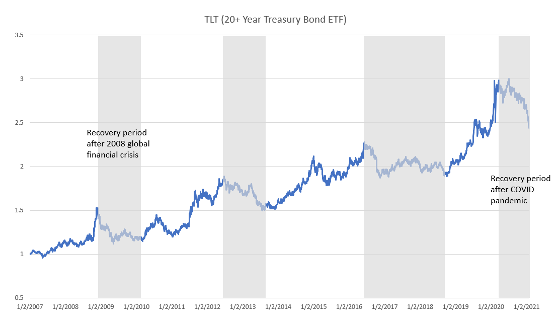

ACM research shows that a 6 to 12-month decline in bond prices is not unusual after a market correction. In fact, both recent and long-term history statistically show that US Treasuries are resilient: Bond prices do eventually recover after each major market downturn. See the below price graph of TLT ETF (2007 to 2021).

Source: ACM Research

A second statistical observation is that after a major economic downturn (e.g. 2008 Global Financial Crisis), Treasury bonds tend to experience depreciation in value for a period as the market recovers. The recent case in point: US Treasury Bond prices have been experiencing a similar drop (Jan to May 2021) as the Feds engage in money printing as part of the US federal fiscal stimulus.

Now, the conventional fund manager might well have access to this data and arrive at a similar interpretation. But where investment philosophies diverge: While a conventional fund manager might make the subjective decision to rotate out of bonds (let’s hold cash or seek a safer haven), a quant fund manager might lean into a non-emotional, non-discretionary process: Statistically, bonds will recover to serve as a worthy hedge, attempting to time a recovery is a fool’s errand; trust the statistical process to capture long-term gains.

This latter scenario gradually panned out in June as bonds recovered – nudging AQM to a new highwater mark.

____________________________________________________________

The curious investor

Every individual’s investing journey and level of engagement is different. For the curious investor, here are some topics for consideration:

- Long and long/short are the dominant investment styles. Most investors can easily relate to a long or long/short fund. How is a multi-strategy fund different and what are its benefits?

- Follow the evidence/data. Try to recall last week’s financial news or last quarter’s news. What does the lack of a coherent narrative across the market tell us? Even seasoned investors struggle to discern the ebb and flow. How does a quant fund filter out short-term noise to get at long-term signals/gains?

- A large drawdown is hazardous to wealth. A fund that delivers 7 percent annual return and experiences 50 percent drawdown will take 11 years to recover; a second fund that delivers a similar 7 percent annual return but, having downside protection, 15 percent drawdown will take only 3 years to cover. In the great game of investing, defense is just as, if not more, important than offense. How does AQM offer upside participation and downside protection?

- Why a quant fund? Ask about the nature of risk-adjusted returns. And why a quant fund is complementary to say private equity holdings in one’s portfolio.

____________________________________________________________

Summary

What does all this mean for AQM investors during this period?

First, be aware that AQM is an equities-driven, not a fixed income, fund. Do not divide 25 percent CAGR by 12 months. A 25 percent annualized return is a long-run target. i.e. The long-run annualized return of bountiful years and a few average years gets us to 25 percent CAGR. Expecting a clockwork 2 percent monthly return (25/12) conflates the nature of an equities-driven fund with that of a fixed income fund.

Second, performance drivers (and detractors) are period-specific, hard to predict, and unlikely to be repeated. In hindsight, the above bond story is a tidy narrative. However, we cannot foretell what future market conditions or asset classes will cause the fund to experience a flat cycle. Given time, drivers and detractors are clear; whilst in the weekly and monthly trenches of investing, we trust our rigorous process.

Lastly, we believe that the meeting of a sustainable, resilient investment process (we humbly think that AQM is exemplary) with sustainable investors (education is critical for attracting long-term investors) leads to long-term, mutually-beneficial performance.