In 1944, two psychologists showed their students a simple animated film depicting a big triangle, a small triangle, and a little ball moving in and around a rectangle.

Overwhelmingly, Fritz Heider and Marianne Simmel’s students felt the big triangle was bullying the other shapes, imagining their emotions, and even constructing a plot around the movement.

This simple yet insightful experiment illustrates that humans are hard-wired to see causality and find narratives – even when the moving objects are simple geometric shapes.

From an investing perspective, investors inevitably craft a narrative to make sense of the market and to rationalize their decisions.

For instance, most investors might scan an annual Top 50 fund list and decide to invest in the top three funds or judge a fund by its recent past performance – what goes up, must continue going up, right?

Well, yes and no.

Yes, because momentum investing is a legit investment style. Think of it as the proverbial bet on the frequently winning horse, choosing to ride the escalator that is going up, and putting money on the player with the hot streak. (Professional momentum investors do apply a strict set of rules based on technical indicators, not simply buy and sell using gut feelings.)

No, because chasing returns by switching investment styles – moving in and out of a fund based on where you think it is headed – epitomizes trying to time the market.

____________________________________________________________

“Most of the time when you see people chasing returns, it’s all in vain. The numbers they’re chasing provide almost no information at all. Think about all those investors who leave a hedge fund after six months because their returns have been bad. That’s the dumbest thing in the world. Six months of returns tells you essentially nothing about the manager’s skill or future returns.”

-Kenneth French, Roth Family Distinguished Professor of Finance at the Tuck School of Business at Dartmouth College, CFA Magazine (PDF 2005)

____________________________________________________________

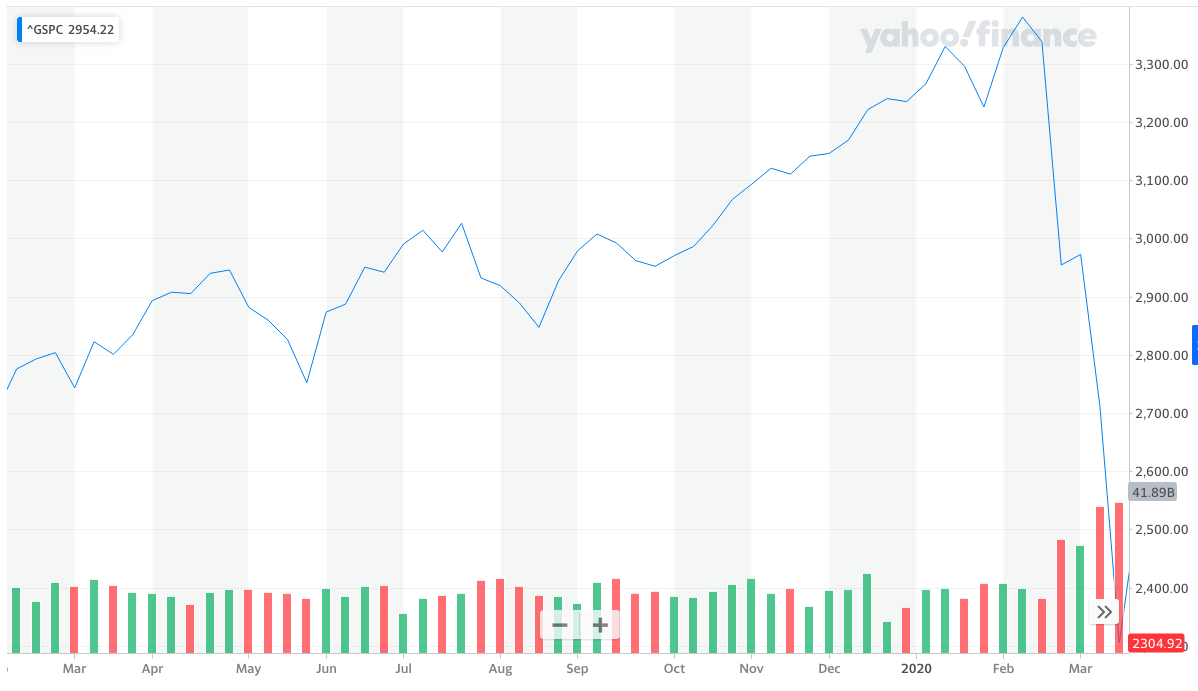

We have a deep-seated desire to see patterns and story create. Take this 12-month graph of a fund: Where would you bet that it is headed next? Up or down?

Source: Yahoo Finance

Answer: Down. Way down.

The above graph was the S&P 500 climbing to an all-time high from Feb 9, 2019, to Feb 10, 2020.

The below graph is the S&P 500 taking a nose dive of negative 20 percent between Feb 11, 2020, to Mar 17, 200.

Source: Yahoo Finance

The point is that by simply looking at a simple graph, we are wired to extrapolate — which is counter productive when it comes to investing.

Another takeaway is that trying to time the market is a fruitless exercise: A recent WSJ article points out that moving in and out of stocks not only lowers returns, it adds to volatility.

____________________________________________________________

Folly of Chasing Short-Term Gains

Though the statistical edge and real-world benefits of proven, time-tested strategies, such as trend following and momentum investing, are quantifiable and simple yet effective once explained, majority of investors will find it a challenge to stay invested in any given investment style for an extended period.

In fact, studies into investing behaviour has shown that investors tend to chase after short-term returns and switch from one investment style (or product) to another when their current investment suffers from temporal underperformance.

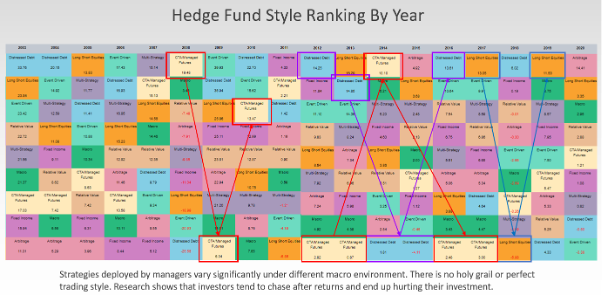

Furthermore, studies show that when a particular investment approach excels in a certain macro environment, it tends to underperform the following period/year when the macro environment changes. See the below Hedge Fund Style Ranking table.

Hence, investors who chase after short-term returns are likely to see their portfolios suffer over time.

Source: ACM Research

To that end, blending investment styles may protect an investor during uncertain times and improve the resilient of a portfolio.

____________________________________________________________

Summary

As Buffett pointed out, “Investing is easy, but not simple.”

Similarly, fund selection is easy, but not simple.

A proper due diligence involves looking beyond backtest results and past recent performance. By applying best effort to understand the Portfolio Manager’s investment philosophy and characteristics of the fund (under various market conditions), product knowledge informs the investor’s narrative which is particularly helpful during stressful, turbulent periods.